Overview of "Will Trump’s shipping insurance plan work?"

This episode of NPR’s The Indicator from Planet Money examines a bottleneck in the Strait of Hormuz caused by skyrocketing marine "war" or political-risk insurance costs tied to the Iran‑related conflict. With many vessels effectively stuck, global energy and commodity markets are feeling the impact (oil briefly topped $100/barrel). The show explains why insurance — usually a low-profile part of trade — has become a central constraint, summarizes President Trump’s proposal to have the U.S. International Development Finance Corporation (DFC) provide reinsurance, and assesses whether that plan can realistically reopen the strait and lower prices.

Key takeaways

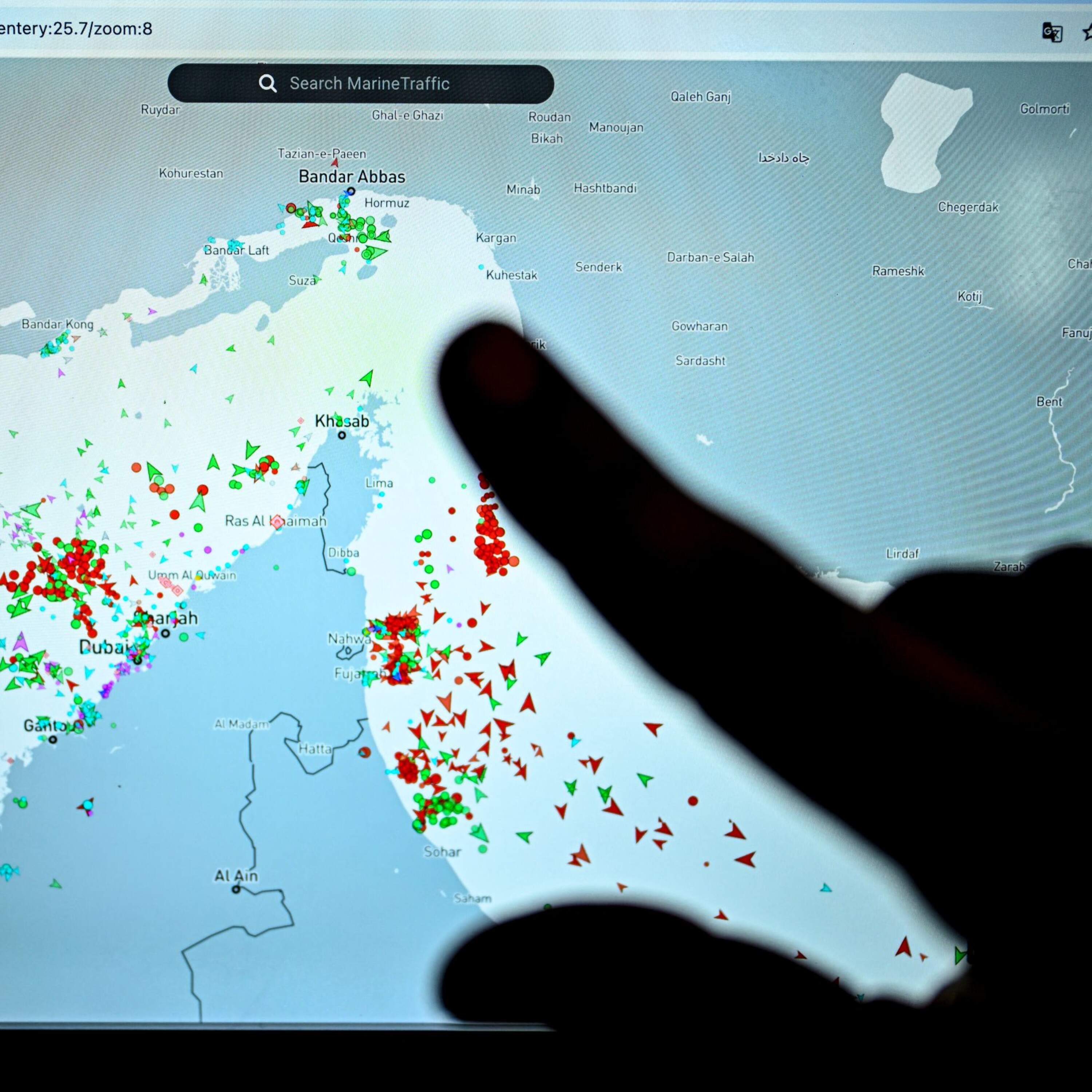

- More than a thousand vessels are delayed in and around the Persian Gulf; many avoid transiting the Strait of Hormuz because of attack/seizure risk and sharply higher war-insurance premiums.

- War-insurance premiums have jumped from basis points to double-digit percentages of cargo value. Example: a $100M tanker passage went from ~$250k to at least $1M for a single day.

- The Trump administration proposes using the DFC to provide up to $20 billion in reinsurance to reduce insurers’ exposure and encourage insured transit.

- Major limits and unknowns remain: which risks are covered, pricing, contract terms, exclusion of crew and environmental damages, insurer willingness, and the speed at which DFC can operationalize the program.

- Security on the water is still crucial. Insurance alone won’t suffice if shipping remains exposed to low-cost asymmetric threats (e.g., naval drones).

Background: Why ships are stuck

- Strait of Hormuz is a critical global chokepoint for oil, gas, fertilizer and other goods.

- Vessels are deterred by the risk of attack, seizure, or other political/war risks tied to Iran-related hostilities.

- Insurers are charging much higher premiums (political-risk/war insurance) for transit; many legitimate shippers decline to pay or to sail uninsured.

- Some ships still transit, but often those involved in shadow/illicit trade that historically operated without insurance.

How the insurance problem works

- Marine war/political-risk insurance is supplemental to standard hull/cargo policies and kicks in for events like missiles, seizures, or detention.

- Normal premiums are expressed in basis points; current market conditions have pushed them into double-digit percent territory for high-risk passages.

- Insurers face potentially huge liabilities (including environmental remediation for oil spills), which drives pricing and capacity constraints.

- Reinsurance (insuring insurers) is a way to add capacity and spread risk.

The DFC proposal — what’s being offered

- The U.S. International Development Finance Corporation (DFC) would act as a reinsurer, offering up to $20 billion in reinsurance capacity to back private insurers willing to cover ships transiting the strait.

- DFC has done reinsurance-like backstops before (e.g., partial coverage tied to Ukraine-related products), but is not primarily an insurer.

- Administration messaging suggests “very reasonable price,” but rates ultimately will be set by private insurers, not the government.

- The DFC proposal reportedly would cover hull, machinery and cargo — but not crew safety or environmental damages (e.g., oil spill cleanup), which can cost up to ~$1 billion per ship.

Main concerns and limitations

- Unclear contract details: exact terms, exclusions, limits, pricing methodology, claims processes and speed of implementation remain vague.

- Insurers may still charge high premia or refuse coverage depending on perceived risk and fine print.

- Excluding environmental and crew coverage leaves significant exposure unaddressed — and taxpayers would back DFC losses.

- DFC lacks deep practical experience underwriting maritime war risk at scale; putting contracts together quickly is complex.

- Even with reinsurance, shipping will only resume if insurers and operators judge the route sufficiently safe — requiring credible security improvements.

Security and long-term risk factors

- The U.S. Navy/coalition security posture matters: demonstrated ability to protect shipping will lower risk perceptions and premiums.

- Iran’s asymmetric tactics (e.g., low-cost naval drones or small craft attacks) make complete security difficult; such threats are cheap to deploy and hard to eliminate.

- The presence of uninsured, illicit vessels complicates the risk landscape and indicates some trade will continue outside insurance markets.

Market impact

- Supply disruptions are already affecting oil, natural gas, and fertilizer flows; oil spiked above $100/barrel briefly.

- Higher fuel and commodity prices are likely while the strait remains risky and shipping capacity is constrained.

- If DFC-backed reinsurance convinces insurers and carriers to resume normal routes, it could alleviate short-term price pressure — but timing and effectiveness are uncertain.

Notable quotes

- “I would describe it as a parking lot…pathways that are frozen.” — Rachel Siemba, Center for a New American Security, on current traffic in the Gulf.

- The administration offered the DFC “at a very reasonable price” to backstop war insurance — but “it’s the insurance companies that will decide how much to charge,” per experts.

What needs to happen for the plan to work (practical checklist)

- DFC must finalize clear contract terms quickly: covered perils, limits, exclusions, claims process and pricing framework.

- Private insurers must be willing to underwrite at prices that encourage shippers to transit.

- Address major coverage gaps or provide parallel arrangements for crew and environmental liabilities (or a separate governmental backstop).

- Demonstrate credible maritime security (military protection/deterrence) to reduce asymmetric threats and lower long-term premiums.

- Rapid engagement with reinsurers and market actors to operationalize capacity in days to weeks, not months.

Bottom line

DFC reinsurance could meaningfully increase insurance capacity and encourage some insured shipping to resume transit through the Strait of Hormuz, easing commodity pressures. However, significant legal, pricing, coverage, and security hurdles remain. Insurance alone won’t reopen the strait unless maritime security improves and contract details convince insurers, shippers, and markets that the route is acceptably safe — otherwise taxpayers could shoulder large losses for a program with limited practical effect.